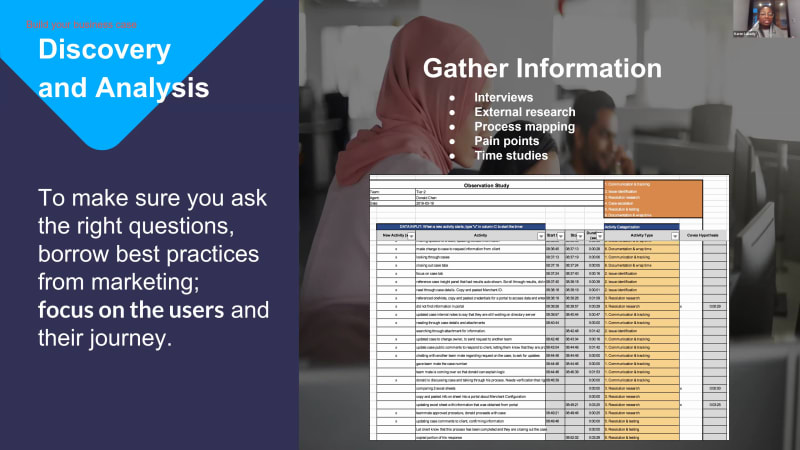

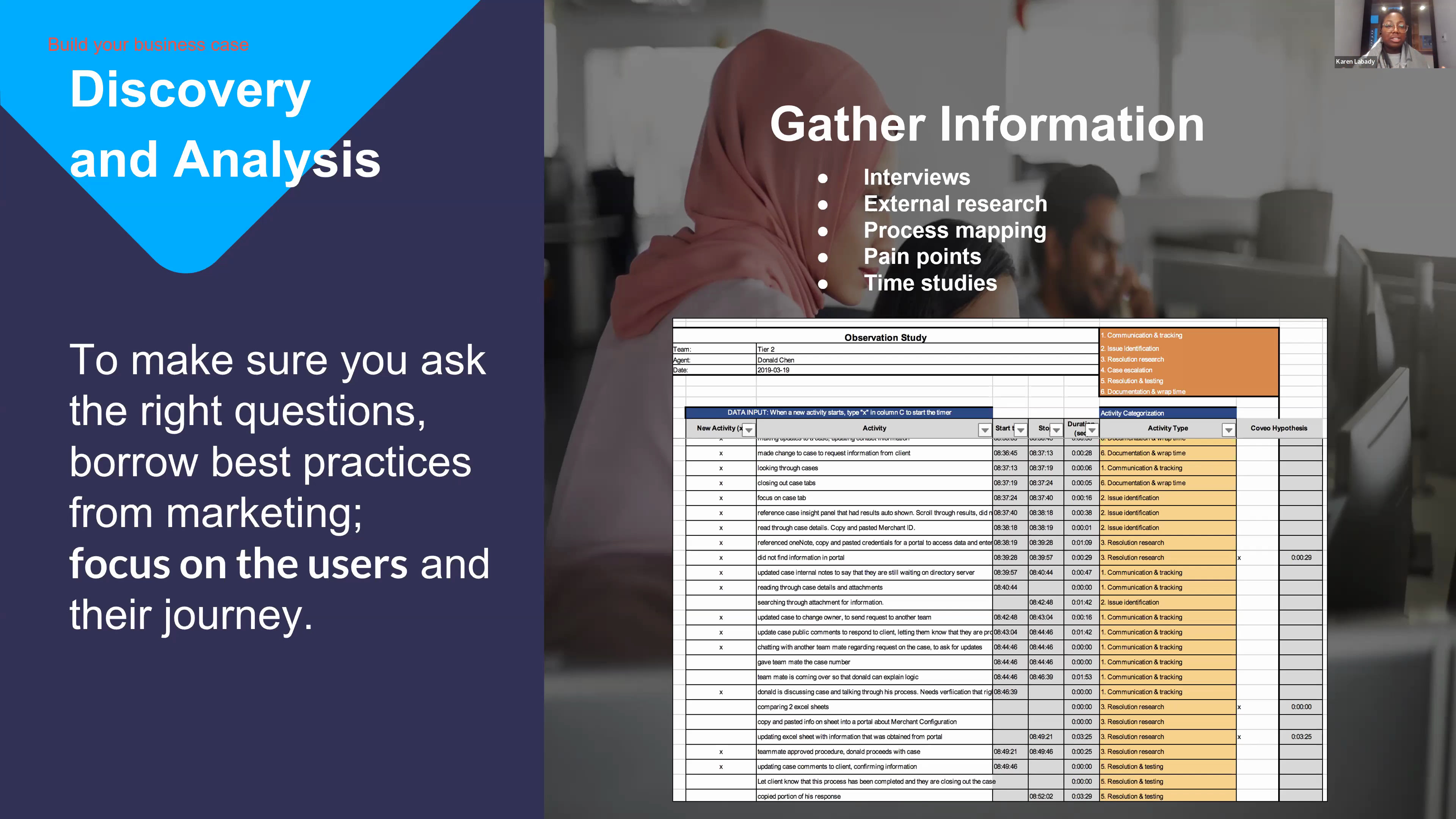

Hi, everyone. Thank you for joining our webinar, building a solid business case for investing in AI powered experiences and financial services. My name is Maggie, and I'll be your moderator today. I'm really excited to be joined today with Karen Laverty. She's our business value consultant. She'll be covering a data driven business use case, and I'll pass that over to you, Karen. Thank you for this introduction. So today's webinar is centered around how to build a data driven business case for financial services. If you are attending this webinar, you might be in a financial services, insurance, or banking, or you're looking for a relevant solution like Coveo. You might also be looking for a framework to help you build a business case for a tech investment, or you might be here to learn about best practice to let you know you are you are at the right place. My goal is for you to leave this webinar with a clear guideline on how to justify investments, whether you are in banking or PNC, and I'll make sure to cover basics with contextual examples in both sectors. You will have a better understanding of some of the value drivers uplift you can expect to achieve with Coveo solution as well. So to continue with our agenda. In this webinar, we will talk about how customers' expectations are shaping the industry. By understanding this shift, we will be able to articulate how to anchor your targeted business outcomes to data evidence. We will continue with how to build a business case step by step, and I'll introduce our business value practice at the end. I'll wrap it up with a q and a. This webinar is about thirty minutes long, and I'll make sure to leave some minutes at the end to answer questions. Just a side note here before we get into, the webinar. I will refer to property and casualty as PNC just to make it shorter. So let's start this webinar with a loaded question. How have customers' expectations transform the digital journeys. We are redefining what has become the new standard, what we want, and how we want it. The customer wants services customized to their ever changing needs, whether it's working from home, commuting more or less, new homeowners, level of physical activities. The list could go on here. In P and C, there is an abundance of personal data steal it away in multiple systems such as CRM, knowledge base, document database, procedure and policies repositories. In a high value center, it can be hard, very hard for customer service agents to handle customer calls as they have to navigate through all those system constantly. Some of our clients in the industry are actually experimenting this. They have the data, but now what? How do we connect the dots from our customers, our customer service agents, and our workplace, the Internet? With the increased flow of the digital channel, users expect more than ever for their online experiences to be fully relevant to them and their journey. In recent reports, clients are inclined to give more of their personal information if they feel like they will benefit from it. That's logical perfectly logical. If we give our information to companies, we want to be rewarded for it. In retail banking, clients want the same experience, do common banking tasks as if they were visiting a branch but without leaving their house. This is our new reality. You might notice as a company within, on the other side that there is an increase in call volume. Customers want quotes based on their new habits, whether it's lower consumption rate, lower risk because their level of activities has changed. Have changed, I should say. So saying that more than eighty percent of customer interaction with insurance firm is digital is absolutely it's making sense. This will have an impact on your business. Being relevant at every touch point is no longer a nice to have approach or feature. It is a requirement to remain alive. The lack of ability to transform and shape your business to customers' expectations will have an effect on retention. That's for sure. This is why we are seeing an increase in insurtech, fintech company, as well as as nontraditional competitors in the marketplace right now. Their business model is centered on embedded technology at the core of operations, whether it's payment process, communication with their client, claim processes without having to support traditional infrastructure cost. Did you know that more than fifty percent of customers would buy insurance from big tech and other nontraditional players according to Capgemini reports? Needless to say, it is imperative to deliver value to your customers. It has to be the driving the driving force behind strategic decisions, including investments and tech. So as a business, how do you go about it proactively? This is the dollar minimum question here. You'll want to build a business case that would address that. You have to define your desired business outcome beforehand to guide you. Here, I've put it together three business outcomes you might want to take a deeper dive into. You have increasing revenues, reducing expenses, and improving experiences. If we start with the first one, your approach could be to focus on increasing revenues through your brokers. It is often an area of the business we don't explore enough when strategically speaking, it might be the asset that you could benefit the most out of. We are currently working with a client that is exploring this, actually. The goal is to understand what is making brokers or teller tellers select your product over a competitor. Assuming you have a partner portal here, how can you showcase your products better? Increasing wallet share is a key in the insurance world as well. Remember, you have a lot of data. With the right tool, you can customize recommendation. Let me give you an example here because I I keep talking, but I think an example is going to solidify what I'm saying. If I am a client who applies for, let's say, a mortgage insurance or mortgage insurance. You know I am a new homeowner. By my age, you can probably tell that I'm it's my first time buying a home. And I'm most likely, I need guidance and product recommendation to further protect what's probably today the biggest investment of my life. This is where we can go from selling one product to growing my wallet share with other well fitted ones. When it comes to reducing expenses, we can also decide to go about it internally. One common challenge for the financial services industry is streamlining operations like claim management. We know it requires a customer centric approach, meet the client where he is, and understand what is he trying to accomplish before he can even articulate his need. This is completely different from just answering calls. It requires access to an overall knowledge. When you equipped your agent with an overview of the customer journey, the interaction with the customer adds value because it is a personalized one. It delivers a sense of understanding and empathy for customers. On the other hand, customers often have a do it yourself approach. We call it a self-service and, do it yourself behavior. They want to be able to manage and perform task without having to rely on business hours, specific channels, or specific advisors. This is where enabling self-service can be your key to reducing expenses by reducing repetitive low value tasks. More than seventy percent of customer expect a multichannel experience for policy research and purchase. This is huge. And this is where you can benefit and have some gain. Improving experiences is rooted in solidifying your user space by improving digital journeys. This is where you might want to focus your energy on if you are a business that is in a more mature stage. This means you are ready to create a unified experience. In the PNC, you have in a position, I I mentioned two seconds ago, a wealth of information, whether it's website tracking, system of record, Internet of things, and more. I've touched base a little on this previously. We've seen in the industry right now how intelligent devices are contributing to sharpen capabilities to assess and price risk right. There is an interest to share health consciousness efforts in exchange for incentive incentive, sorry, like personalized interest rate. How are you using this knowledge to tailor recommendations to your customers? Another I'll give you another example here. If I have a client in Chicago, I want information that apply to Chicago, to my location specifically. So having to go through info regarding other states is creating friction for me. I don't understand why. Consequently, my self ex service experience is not one that I wish to repeat. One example of that would be one of our client internally that we're working with in cloud banking. That client, because of, the business model he chose, enabling self-service was a key success factor for that business. For that client, self-service success meant making the information findable regardless of the channel cost the customer chooses. Customers were browsing less pages, but they were spending more time reading knowledge article. That's a huge game. Internally, in your workplace, you want to have it at your disposal what is relevant to your position, your branch, whether it's task specific or role specific information. You might be in a situation where the intranet is the central link to employee across the globe. You won't have the ability to communicate efficiently and fast. So those are the three business outcomes we are going to touch base afterwards when we talk about value drivers. So now where are we? We've assessed what business outcomes speak the most to your context. You are looking at purchase purchasing something that can fix that, but you need to build a business case for it. This is what we are going to talk about. Building a business case will help you get investment. When done right, it will help you to get people on board and track value over time. This approach here that you probably see on your screen is borrowed from our practice. We use it to assess our clients. So step one is to ask the right questions. And you want to focus on the user. This is crucial. I can't stress that enough. This is the foundation of the business case. Step two comes after you've completed your analysis. You want to make sure you tackle the potential solutions and present recommendation using the right framework. We'll dive into that one, especially around business value drivers. The step three is around the feasibility of software investment. What is the total cost of ownership? Additional risk cost. It might also open the door to a build versus buy conversation. The step four is to socialize and improve your thought process. You'll want to get feedback from key stakeholders before you move to the final recommendation. And finally, step five is to make sure that the business case is a living, breathing document by updating it and align goals, incentive for stakeholders and users. When you think about it, your business case should provide financial justification and define how success will be measured over time. So let's jump right into it. The first step is discovery and analysis. This is your baseline. We need to establish the current, the as is situation to be able to report on it later. First thing first is to identify the key issues we want to have an impact on. All companies are not on the same level of awareness. So to make sure we ask the right questions, it's important to borrow the best practices depending on the context you're in. Just like in marketing, it's important to focus on the user and their journey. Your user could be your customer, your agent, your broker, your tailor. If you don't know how to get it started or what to prioritize, I like to give the example to to client. Think of it as a funnel. Don't rule out information right at the beginning because you don't know. Gather as much information as possible by conducting interviews, looking externally for best practices, map out your current process and what has changed lately, identify the key pain points, and conduct time studies to understand where some backlog is coming from. If you're looking at the support use case, our starting question could be, where are your agent spending or wasting time nowadays? In our practice, we use a tool called Dilo, d I l o, and stands for date in the life of and your position and your type and your title. We shadow basically, what it is, we shadow a user to understand what is involved in handling, let's say, an issue or a claim. Why are we doing this, you might be asking. The goal is to structure the information, understand the current state, and build assumptions around different journeys and understand how they are overlapping in some areas. Then you want to boil it down to use cases. As we are talking about tech investments, it needs to answer a specific use case just like any other investment. So now we've talked about discovery and analysis. So far, we've defined what ROI component we are focusing on. We gather information to help us identify areas of opportunity. We also validated some of use case for, for tech investment at a strategic level. So what's next? You want to confirm your users' need. Think of this as you're delivering a new product to your users. Have you considered the most and important needs? Are they in priority? Does solving them serve the bigger picture? Do you have a narrative on how it is supporting daily operations? Once that is defined, you'll want to link the investment to specific business objectives. You want to support that within the overall strategy. We want to be able to frame the story before getting into numbers. And finally, you'll want to identify value drivers that will serve as a baseline. To achieve your business outcome, value drivers are what is going to help you quantify your efforts financially. Those inputs are going to be used to calculate the ROI later on. So we've established our framework. How do we link business outcomes to financial benefit? This is where we're gonna talk about value drivers. This is where they come into play. This is something that we work with day in and day out in our business value practice here at Coveo. The goal is to identify the areas of value creation or cost avoidance to make sure that our clients' investment in technology is solid and more so financially sound. Now we've identified business outcomes you'd like to tackle. We need to define what value drivers are going to be the most impactful. Once we do that, we have to come up with how we can measure it. And from that point, forecast improvements and calculate financial impact annually. I've identified some value drivers that we address to p and c retail banking. They apply to different use case. But when you do this exercise internally in your company, use value drivers that apply to your use case specifically, the ones that are going to have the most impact. So I separate the, value drivers, with the business outcomes. So if your goal is to increase revenue, looking at AUM is logical. Asset under management, AUM, could be further breakdown per broker, per adviser, per teller as it is related to wallet share. How are you leveraging broker retailers to suggest to suggest your product over your competitor? Is the solution you're thinking about compatible with your partners? In p and c, we could think of a similar ratio such as sales growth rate, let's say, With the nuance here of new policies versus renewals. It's going to give you a better idea of how your company is performing internally. If you wanna take the second approach, which is producing expenses, we can link productivity to the average time to close an issue. Can the solution help reduce time waste? In financial services, every detail matters. Let's say, in banking more specifically, you have a customer calling for a loan. There is a lot of back and forth. Customer might throw in information to the agent on the other hand that that person cannot, categorize right away the information. He might put the client on hold, ask to a colleague, search on the requesting system. This can happen multiple times. Search plays a huge part in the average time to close. You need to ask yourself, is the solution addressing that? I also want to give you some value drivers for retail banking. Looking at operational inefficiencies might be a beneficial way to look at it. We could identify new accounts, set up error, or insufficient documentation. The first one is when the client provide data that is incorrect. It could be as simple as, a typo, the type of account selected or the wrong address. Whereas, the new account with insufficient documentation, here the data is missing. In terms of total volume accounts, it can become very costly very rapidly. Do you do you understand where I'm going with this? If you're not equipped internally to detect and correct those. Providing the right tools and a personalized approach supported by tech can accelerate your agent's time to proficiency. What does a day or fifty hours saved in onboarding time means for your company? Are you in a growth management mode? It's possible there might be a merger and acquisition discussion floating around. How the manager how the management team is going to navigate through the workforce activity post merger is something to think about. When we talk about improving experiences, I'm referring to client and employee advisors or teller. With all of the previous drivers in place, how is it affecting clients? More specifically in a financial services industry, we would look at policy renewals. We could look at retention, referrals rate. On the other hand, if we're talking about advisors satisfaction, with better tools in place, you're enabling you're enabling advisors to become more efficient. You're giving them the ability to reach quote rate, quote rate way faster. So when it comes to baseline, the biggest challenge, we often get that question when we embark on a journey with a with a client. How do we build a baseline? Not all client have the same level of granularity when it comes to operating data. It's a comment. Here at Coveo, because we deal with companies like yours daily, we are able to use anonymized customer performance metric to measure you against. When it comes to KPI improvement, it is important to figure out what is the improvement hypothesis. But also how to track this over time. Do we need to build analytics tools? Is the solution that we're thinking about comes with analytics out of the box? Will tracking this KPI give direct benefit? Those are all value drivers that you should keep in mind. Those are great ones. You might have others you track in house. That's perfectly fine, and that's normal. Use those instead as they fit your context already. So now we we've talked about analysis, discovery. We've talked about value drivers. For now, we have to talk about what is required to make it happen. Right? We are going to spend time on feasibility. Now if you look at it, we need to set up cost associated with setting ourselves up for success, whether it's deploying and maintaining. Overlooking those can lead you to not see expected results. It might be delayed. In upfront costs, data migration is important. If you buy a solution, do you need to store data somewhere else while implementing? There is a lot to think about whether you're cloud based or you're on premise or a mix of both. It's possible. Do you need to provide twenty four seven support in some branches? What about IT security and compliance? Those are areas that you need to keep in mind if you want to take the job. And deployment cost, it is done. Is it done in house or through a partner? Key question would be how to integrate with the right features. What should I unlock first? In ongoing cost, pricing models have to be considered right away in the beginning because you want to figure out what is your consumption point that is going to be defined. How many line sizes do you need? You need to know that over time. On the higher level, we also need to consider key success factors to support feasibility. One example that comes to mind thinking about it would be change management. I've mentioned a lot of cost here. Now it will have an effect on the ROI. Probably, I'm going to be to tell you upfront, it's probably going to decrease it. But remember, you want your business case to be realistic, for one, in front of stakeholders. This will help you gain credibility and ownership. Now we can talk about feasibility without saying a few words about other possibilities. This leads me to talk about the buy versus build dilemma. The truth is you might be challenged on this internally. Your company might not be set on a solution just yet. It is always worth it to map out the difference between building and buying on a scale of business value versus risk, time to value, scalability, and limitations. Ultimately, the the questions you'll want to ask yourself is, what are the costs, first of all, of building or buying? Do we have the resources? Is the investment in technology a mean to create a differentiation? And most importantly, is it time sensitive? What is our time to value here? Do we need to deploy in two, three months and start seeing results before the end of the year? Or we can afford to delay time to value by one, two, three years by going for a build strategy. The sense of urgency here might not be there, but it's going to be an indicator. The key takeaway is to highlight time to value with an out of the box solution like Coveo versus having to configure, build numerous extension, customize in house. You also run the risk of jeopardizing your ROI with unexpected costs and events. It is something that you want to keep in mind. Now once you've put together your potential benefits and cost structure, you need to build your ROI and net present value hypothesis. Some of the key assumptions to build a solid and a flexible model are define the phase. Do you want to deploy all the features right away or you want a phased approach? Define the adoption rate over time and impact on benefits. The ramp up schedule, like we said earlier. Identify the difference between value creation and cost avoidance. Add some contingency level to to your cost. Use a growth rate if needed. You're probably talking about headcount, sales projection, a discount rate to account for opportunity cost, your key success indicators, payback period, NPV, your ROI, the IRR, internal rate of return. Keep those in mind. You'll be able to build a sensitivity analysis to see how much assumptions impact your ROI. So the the step we're gonna talk about, this is the one of the step that I like to talk about it because it's obtain the buy in, how to involve people, how to gain adoption. So to gain adoption for your business case, you'll need to obtain business partner support and executive sponsorship throughout the organization. Validate with your business partners that the business case is solving, in fact, the right problems. The step one discovery analysis is going to help you frame the story you wanna tell in a more cohesive way. The methodology we use here today within the webinar is to build our business case and putting together business outcome to major value drivers. So it's always a recipe for data driven results. Don't be scared to iterate to get it right. The more you include stakeholders, recommendations, the more buy in you will get. And once you're done and you're able to present, the last step, but not the least, is to update. A business case, I mentioned this within our intro today, is a living breathing document. It's an asset and not a document that you want to shelve once you've presented, and obtained budget for it. Use your business case as a guide to manage value realization and understand where we can improve as your business is constantly being challenged. When you report on value over time, it will become inevitable. You want to continuously join. So because you are building a framework for success at every time. So we are at the end of our webinar. I'd like to take this moment to talk about the business value practice and what we do. To date, I believe we've completed more than probably three hundred business value assessment and value realization. The purpose of this practice is to help clients build success plan that they can report on over time. We help oh, I went too fast here. Apologies. We help you build a business case to make sure that you look at your best, but you considered all the important aspect within building a business case. I also want to make sure that you take the time to look at other webinars we have in our online library. We go into further details and break down building a business case per use case. So it might be your next step. I'm inviting you to engage with us. I believe there will be a link to contact us to get this started. So we will continue with our q and a. So back to you. Hi, Karen. Thank you. That was amazing. I hope everyone found a lot of value out of that. It doesn't look like we have any questions at this time, but thank you everyone for joining, and we will follow-up with you soon. Thank you, Karen.